Iran Conflict & Wealth Risk: A Family Office Guide to Risk Diversification for Malaysian HNW Families

What the 2026 Middle East conflict reveals about single-country wealth strategy — and how Malaysian family offices can build resilience across jurisdictions

The 2026 Iran conflict is a live demonstration of why risk diversification across jurisdictions has become central to modern family office strategy in Malaysia. When wealth, banking, and assets sit too heavily in one country, the bigger risk isn't a market crash — it's losing access to your own money when borders, banks, or regulators tighten overnight. This guide explains why concentration risk matters now, how the Forest City SFO scheme changes the equation, and what a resilient multi-jurisdiction family office actually looks like.

Why This Matters Now: The 2026 Wake-Up Call

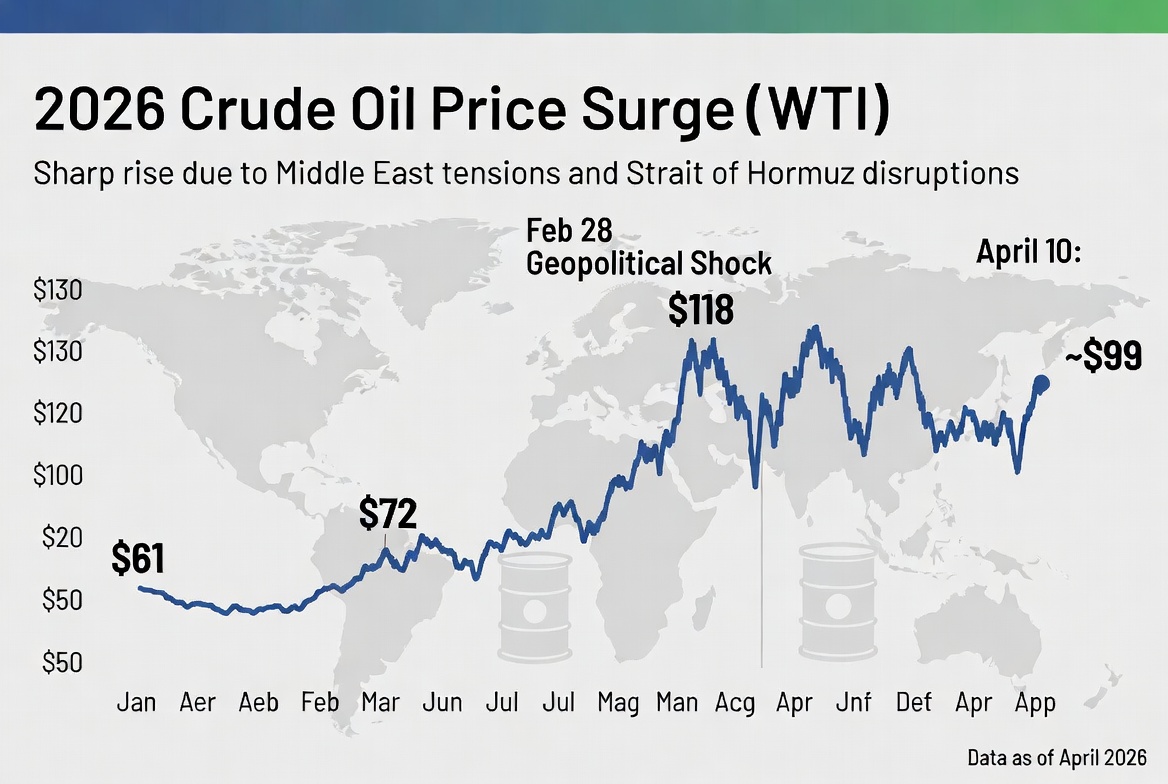

On 28 February 2026, joint US-Israeli airstrikes targeted Iranian leadership and strategic infrastructure, killing Iran's Supreme Leader and senior military commanders. Iran retaliated with missile and drone strikes on US and Israeli targets — and on Gulf states hosting US forces — leading to airspace closures and direct damage to infrastructure in Dubai, Abu Dhabi, Qatar, and Bahrain.

For Malaysian families who had been placing capital into Gulf property, banking, and business setups, the implications were immediate. The very hubs marketed as "safe" and "tax-friendly" were suddenly under physical and financial stress. Banks tightened compliance reviews, transaction processing slowed, and the property market lost buyer-side depth overnight.

Not Theoretical

Iran's rial has lost most of its value, inflation runs near 40%, and at the height of recent unrest, ATMs went offline and currency transactions were suspended. These conditions show how quickly a functioning financial system can become inaccessible — and how the fallout spreads to neighbouring hubs that handle the regional money flows.

The Real Risk: Loss of Access, Not Loss of Value

Most people think wealth risk means a market crash or a property downturn. Those are real, but recoverable. The risk that family principals consistently underestimate is more subtle: you still have the money on paper, but you cannot reach it. A regulatory hold, a frozen correspondent banking line, a closed border, or sudden capital controls mean you cannot move, spend, or deploy your wealth when it matters most.

Frozen Banking Lines

Even a 60-day compliance review can derail a property closing, school fee payment, or business obligation. Your balance doesn't change — your ability to use it does.

Illiquid Property

Real estate that looked stable cannot be sold when buyers vanish. A "liquid" market in February can turn into a six-month ordeal by March.

Capital Controls

Sudden restrictions on outward remittances or FX conversion limits trap working capital exactly when the family needs flexibility most.

In each scenario, the family isn't poorer in an accounting sense. But operationally — the ability to act, protect dependents, or seize opportunities — they are temporarily powerless. That is what risk diversification across jurisdictions is designed to prevent.

The Malaysian Reality: Too Many Families Are Single-Basket

From what we observe across the Malaysian HNW landscape, a remarkable number of families remain heavily concentrated. Common patterns include: the overwhelming majority of net worth held inside Malaysia through operating businesses and property; meaningful offshore capital sitting in one location only (often Dubai); reliance on just one or two banking relationships across the entire family structure; and international assets denominated in a single foreign currency.

Each pattern is understandable — they reflect existing relationships and trusted advisors. But each creates hidden concentration risk that only becomes visible when something goes wrong.

The Three-Question Test

First: if your primary banking jurisdiction imposed capital controls tomorrow, what percentage of your liquid wealth is affected? Second: if your secondary jurisdiction did the same, what would still be reachable? Third: how many days of family expenses can you cover from assets entirely outside both? If the answer to the third question is fewer than 90 days, your structure has a concentration problem.

The Family Office Answer to Concentration Risk

A family office is the operational answer to concentration risk. It serves as the coordinating layer that ties together multi-jurisdiction banking, legal structures, investment mandates, and succession planning. Without it, each element drifts independently and the family inevitably ends up concentrated in whichever piece grew fastest.

The advantage of a family office — whether a single family office in Malaysia, a Singapore structure, or a hybrid — is that it forces the family to treat risk diversification across jurisdictions as a permanent policy rather than a one-time decision. The family office charter defines how much wealth sits in each jurisdiction, which banks hold operating liquidity, and when the allocation gets rebalanced.

Why Malaysia Is Now a Credible Family Office Home Base

Until recently, Malaysian families who wanted a formal family office had to look to Singapore or Hong Kong by default. That changed with the Forest City Single Family Office Incentive Scheme in September 2024, offering a 0% concessionary tax rate on qualifying investment income for up to 20 years. For the first time, a Malaysian family office can sit alongside Singapore or Hong Kong as a tax-efficient co-equal leg of the overall structure. For a walkthrough, see our Malaysia SFO application guide.

Family Office + Trust: Complementary, Not Competing

A family office provides coordination and governance. A trust provides the legal wrapper for succession and asset protection. Many families combine an approved SFOV with an offshore trust — capturing both the 0% tax rate and succession continuity. See Forest City SFO vs Labuan Trust vs Offshore Trust.

What a Resilient Family Office Structure Looks Like

Risk diversification across jurisdictions doesn't mean leaving Malaysia. It means structuring so that no single jurisdiction, bank, or asset class controls the family's ability to act. A resilient family office typically rests on four layers:

Multi-Country Allocation

Malaysia as home base, complemented by one or two stable international jurisdictions — typically Singapore, Hong Kong, or a Western financial centre.

Multiple Banking Relationships

At least one local Malaysian bank plus an international private bank in a different jurisdiction. Critical accounts should never sit with a single banking group.

Legal Structure Layer

A trust, foundation, or holding company that provides asset protection, succession clarity, and a legal wrapper that survives any single jurisdiction's upheaval.

Liquidity Planning

A defined portion held in instruments accessible within days. Property and long-lock private equity should not dominate the entire balance sheet.

Concentrated vs Diversified: A Comparison

❌ Concentrated

✅ Diversified

The exact split varies by family. What matters is the principle: no single shock can paralyse the family's ability to act. The Forest City SFO scheme makes the Malaysian leg genuinely competitive — the 0% concessionary rate means you no longer pay a tax premium to keep wealth at home.

Geopolitical Shocks: 2020–2026 Timeline

The Iran conflict sits inside a longer pattern. Shocks that once seemed once-in-a-decade now arrive every 12 to 24 months:

Families that built their structures assuming permanent stability in any single jurisdiction have repeatedly had to rebuild under pressure. Families that built for resilience from the start simply absorbed the volatility.

Frequently Asked Questions

Wealth Is About Control, Access, and Protection — Not Just Growth

The 2026 Iran conflict is one event in a longer pattern. The common lesson across every recent crisis — Hong Kong 2020, Russia 2022, Gulf 2026 — is that stability is never permanent. A balanced family office structure with Malaysia as a credible home base, complemented by stable international jurisdictions and proper legal layers, neutralises most of the risks that look frightening in headlines. Most people react after a crisis. Real wealth planning happens before.

Worried About Concentration Risk in Your Family's Structure?

Geopolitical risk, banking concentration, and succession planning interact in ways that need coordinated analysis. Timeless International Family Office supports Malaysian families navigating multi-jurisdiction structuring, SFO setup, trust planning, and resilience-focused wealth design.

Request a Discussion

*Limited availability. Please mention "FIAM Iran War Wealth Risk Guide" when enquiring.

FIAM provides general information only and does not offer financial, legal, or investment advice. Any structuring or implementation is carried out by independent licensed professionals.

References & Sources

- Wikipedia — Economic Impact of the 2026 Iran War

- VinciWorks — Compliance Fallout From the 2026 Iran War

- McKinsey — Asia–Pacific's Family Office Boom

- EY Malaysia — Single Family Offices: A Catalyst for Malaysia

- Bloomberg — Competition Increases for Family Offices Across Asia

- Al Jazeera — Why Is Iran's Economy Failing?